Calculating Cost Savings: Maximizing Savings in 2026

Learn how to calculate cost savings. Our 2026 guide helps you define relevant costs, apply formulas, and identify savings potential.

You are probably sitting on an idea that already makes sense in your company. Maybe you want to move shift planning out of Excel and WhatsApp. Maybe you want to introduce a tool that reduces inquiries, no-shows, and follow-up calls. The problem is rarely the idea itself. The problem is the question from management: What does this actually save us?

This is exactly where gut feeling separates from a solid business case. In events, gastronomy, and other service-based businesses, a “this will probably be cheaper” is not enough. You need a calculation that shows which costs are incurred today, which remain after the change, and which difference actually counts as savings.

If you approach calculating cost savings properly, a good guess becomes a reliable decision basis. And you avoid the typical mistake of only comparing license costs against a vague benefit promise while the real cost drivers remain hidden in daily operations.

Meta description: Want to calculate cost savings and justify a new tool properly? Here you get a practical guide with formulas, examples from events and gastronomy, and typical mistakes from everyday business.

Table of Contents

- Why Your Gut Feeling Is Not Enough

- Identifying the Right Types of Costs

- The Most Important Formulas for Your Calculation

- Example Calculation from the Event Industry

- Collecting Data and Avoiding Typical Mistakes

- Conclusion: From Calculation to Decision

Why Your Gut Feeling Is Not Enough

You know the situation. The team lead complains about too many last-minute changes, the dispatcher spends evenings on phone chains, and after every event there are discussions about timesheets. Everyone sees the problem. No one can say what it costs in Swiss francs.

The Moment Before Approval

At the latest when you request a budget, that is no longer enough. Then someone asks three simple questions: What does the current process cost, what does the new process cost, and when does the change pay off? If you don’t have a clear answer, even a good idea looks like a risk.

Especially in events and gastronomy, the same often happens. People look at the price of the tool but not at the price of the previous improvisation. The real costs lie in planning effort, misstaffing, overtime, finding replacements, double data entry, and delayed payroll preparation. To make this visible, you don’t need a fancy presentation but a comprehensible calculation.

Practical rule: A project is rarely approved internally because of an idea. It is approved because someone has clearly quantified the financial difference between today and tomorrow.

A good start is to map the current process on paper. Who plans? How often are changes made? Where is work duplicated? In companies with many assignments, a look at the daily planning load often helps. If you want to see how digital dispatch reduces friction points in daily personnel work, this article on Reducing Personnel Costs with Digital Planning is a useful complement.

What a Good Calculation Must Deliver

If you want to calculate cost savings, you need more than an estimate. Your calculation must deliver three things:

- It must show the current state. Not “we lose a lot of time,” but which activities consume time.

- It must isolate the change. Not everything that goes wrong in the company belongs in the business case for a new tool.

- It must be verifiable by others. Anyone reading your number must be able to understand how you arrived at it.

You are not selling a tool internally. You are proving that a different process is economically sensible.

That’s exactly why the calculation is not a side job for accounting. It is your lever to secure a good business decision.

Identifying the Right Types of Costs

Anyone who wants to calculate savings properly must first know which costs are actually relevant. In service companies, items are regularly forgotten that seem normal in daily business but are expensive from a business perspective.

Separating Direct and Indirect Costs Clearly

The first separation is simple. Direct costs are directly linked to an assignment or order. Indirect costs arise in the background to keep the company running.

In an event agency, direct costs include wages for hosts, bar staff, stagehands, or drivers. In a gastronomy business, kitchen and service hours belong here, as well as project-related materials or travel costs for an event. Indirect costs include dispatch, recruiting, internal coordination, software, administration, and rent.

Personnel costs are often underestimated. According to PostFinance on calculating personnel costs, in Switzerland you must add a flat 20 to 25 percent for ancillary wage costs on top of the agreed gross salary. An employee with a CHF 13,000 gross salary per month actually costs your company at least CHF 15,600. If you only use the gross salary for a team lead or dispatcher, your entire calculation is too low from the start.

Anyone who calculates planning time only at the hourly wage underestimates the business case.

If you want to get a sense of how much proper budget planning changes the view of ongoing costs, the Work & Travel Start Capital Guide is a helpful model. Not because of the industry, but because it clearly separates ongoing and one-time expenses. Exactly this separation is needed in your company.

Hidden Costs in Events and Gastronomy

The expensive items are often not the obvious ones. They hide between the lines of daily business.

- Training new people: When new temporary staff constantly start in the bar, service, or setup and teardown, it costs the shift leader’s time. This time rarely appears as a separate cost block.

- Last-minute replacement search: If someone calls out on event day, the extra work falls on dispatch or operations management. More expensive spontaneous staffing follows.

- Manual follow-up: Collecting hours from chats, photos of timesheets, and Excel files costs quiet office time. This goes unnoticed as long as it happens “on the side.”

- Error costs: Double-booked people, missing qualifications, or wrong shift times lead to complaints, extra trips, or overtime.

A useful calculation does not list these items under a generic “admin” label. You assign them to specific activities, such as shift planning, rebooking, communication with temps, approval of times, payroll preparation, training, replacement search.

A quick rule of thumb from daily business: If a process recurs every week, it almost always belongs in your calculation.

The Most Important Formulas for Your Calculation

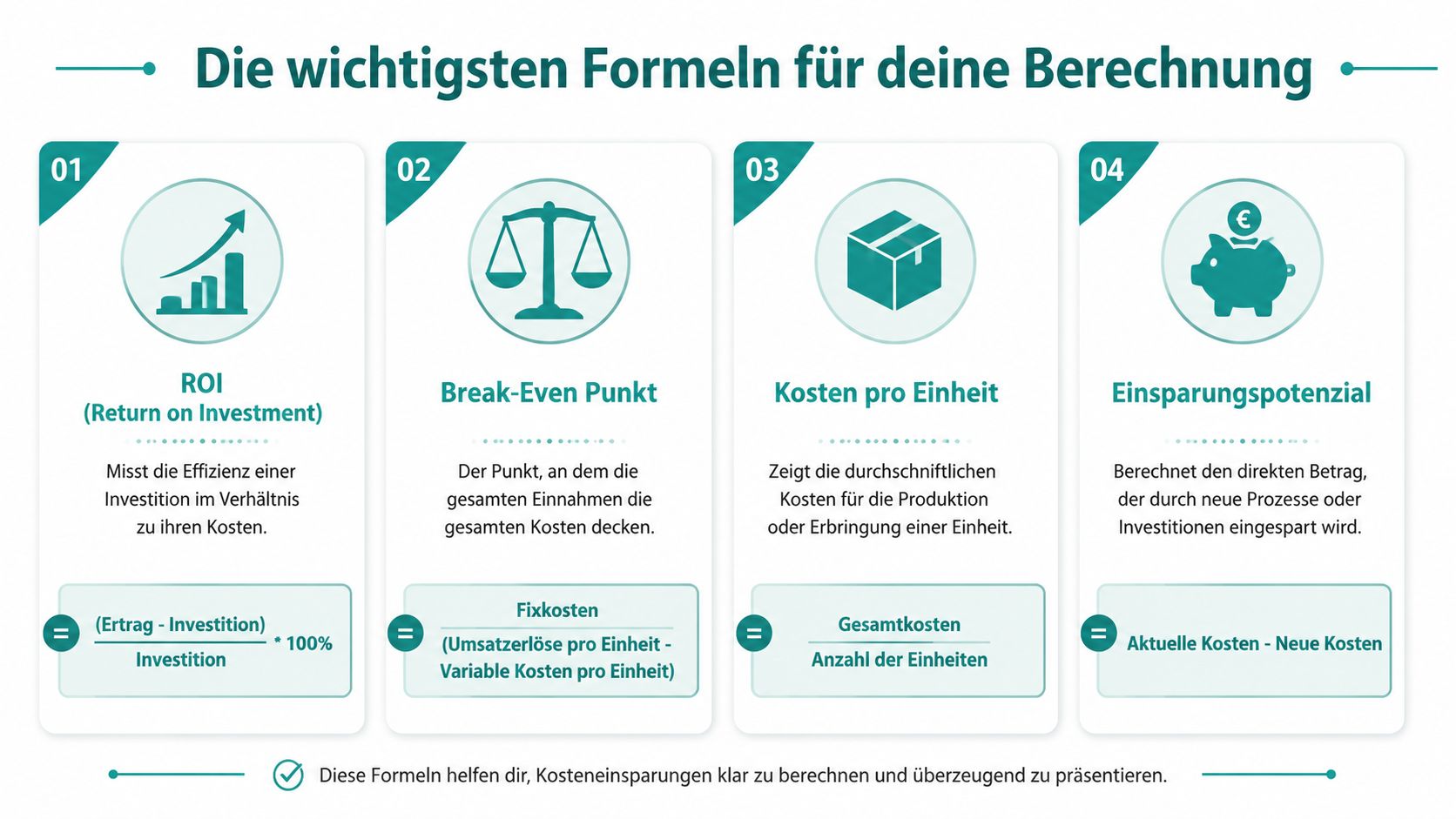

Now we get to the math. You don’t need complicated financial jargon. For a good business case, a few clear formulas are enough as long as you feed them with real company data.

Gross Savings and Net Savings

The simplest formula is often the most useful.

Gross Savings = Current Costs – New Costs

If you currently spend more per month on a process than after the change, the difference is your gross savings. This works well for planning time, printing costs, external recruiting, or manual payroll preparation.

A small example from gastronomy: You measure what branch management currently spends on schedules, last-minute changes, and inquiries. After switching to a clearer process, part of this work disappears. You value the saved time at the actual employer costs of the responsible person, not just the net salary.

Net Savings = Gross Savings – New Ongoing Costs – One-Time Implementation Costs

Here it gets realistic. Many business cases fail internally not due to too little benefit but due to overly optimistic assumptions. If a tool causes license fees, training, or data migration, you deduct these items clearly.

A saving is only reliable when you also offset the new costs.

A practical addition for cash flow in daily business is a clear view of accounts payable and due dates. If your company’s invoices to suppliers, freelancers, and venues are often confusing, this guide to managing supplier payments helps you organize the payment side.

If you still build your current planning with lists, it’s worth looking at this Work Schedule Excel Template. Not because Excel is the final solution, but because it quickly shows which work steps are actually involved in the current state.

Return, Amortization, and Annual Comparison

The next formula you need for approval:

ROI = (Return – Investment) / Investment × 100 %

This formula is standard for investment decisions. In your case, the return is the financial effect of the change, e.g., saved personnel time, fewer error costs, or fewer external assignments. The investment includes license, implementation, training, and internal effort. The graphic above shows the formula for orientation.

The break-even point is also useful if you want to prove when a change pays off.

Break-even = Fixed Costs / (Revenue per Unit – Variable Costs per Unit)

For events and gastronomy, this is not always the first formula. But it helps if you want to show the effect per assignment, event, or shift. If the new process generates fewer variable costs per assignment, you can show from which quantity the change pays off.

There is also the cost per unit formula:

Cost per Unit = Total Costs / Number of Units

The unit can be an event, a shift, a supported guest event, or a staffed assignment. This makes discussions much clearer. Instead of talking about “a lot of effort,” you show costs per event before and after the change.

This video helps to understand the formulas:

When Calculating Over Multiple Years

As soon as you evaluate purchases or longer useful lives, a simple monthly comparison is often not enough. Then the annuity method comes into play. According to EnBau on profitability calculation, investment evaluation in Switzerland often follows this method. Future cash flows are discounted to present value so that annual costs over the useful life become comparable. This approach provides high planning accuracy according to the same source.

For you, this practically means: If you evaluate a tool not just for one month but over several years, you should not blindly compare one-time costs against a single month’s benefit. You spread them over the assumed useful life. This way you compare fairly.

A simple presentation in the business case is often enough:

| Consideration | What You Use | What It’s Good For |

|---|---|---|

| Monthly Comparison | Current monthly costs vs. new monthly costs | Quick preliminary check |

| Annual Comparison | Annual costs today vs. annual costs new | Budget discussion |

| Multi-Year View | Annuity method | Proper evaluation of larger investments |

Example Calculation from the Event Industry

Let’s take a medium-sized event agency. It plans personnel for promotions, trade fairs, and evening events. Dispatch works with Excel, chat groups, and phone. Changes go to two team leads and one back office person.

Agency Starting Point

The problem does not show in a single large invoice but in many small frictions. The team lead re-plans shifts multiple times. Replacement staff are sought under time pressure. Times come back late or incomplete. Payroll preparation drags on because data must be merged from several sources.

The agency wants to switch to a more digital process. Not as an end in itself but to reduce administrative burden and planning errors. This sentence is not enough for management. So the calculation is built on three cost groups:

- Planning and coordination effort

- Costs from last-minute replacements

- Follow-up for time tracking and payroll preparation

Good business cases rarely start with the tool. They start with the most expensive daily downtime.

If you have a similar environment, you will find a suitable mindset for the target state in this article on Personnel Planning in Events Without Excel.

How to Build the Calculation

First, you reveal the current state. Not roughly, but with real activities. An example looks like this:

| Cost Item | Manual (Current State) | Automated (Target State) | Savings |

|---|---|---|---|

| Shift Planning | High manual effort in Excel and chat | Bundled planning in one process | Time saved in dispatch team |

| Last-minute Replacements | Frequent phone chains and extra work | Faster replacement | Less additional effort |

| Time Feedback | Scattered feedback | Centrally recorded times | Less follow-up work |

| Payroll Preparation | Manual checking and merging | Clearer data basis | Less office time |

| Misplanning | Wrong or double assignments | Fewer coordination errors | Less correction effort |

The table deliberately contains no made-up numbers. You must get the numbers from your company. The structure is always the same: Cost item, current process, new process, monetary difference.

For the actual calculation, proceed as follows:

- Record planning time: Measure over several weeks how much time team lead and dispatch spend on assignment planning, changes, and inquiries.

- Apply employer costs: Value this time not with an estimated hourly rate but with the actual full costs of the employees.

- Add error costs: Include additional effort for rebookings, follow-up calls, and corrections in the calculation.

- Include new costs: License, training, and any implementation costs must be included.

A practical example from everyday life: In many agencies, not only dispatch spends time planning. Project management, back office, and sometimes on-site management also catch errors. If you only calculate dispatch, a large part of the truth is missing. That’s why it’s worth assigning every process step to a person.

If three roles each take on a little extra work, it seems harmless. In total, it becomes an expensive standard process.

The calculation goal is not to perfectly predict every small saving. The goal is to turn scattered extra work into a reliable cost picture. That’s exactly how you get internal approval.

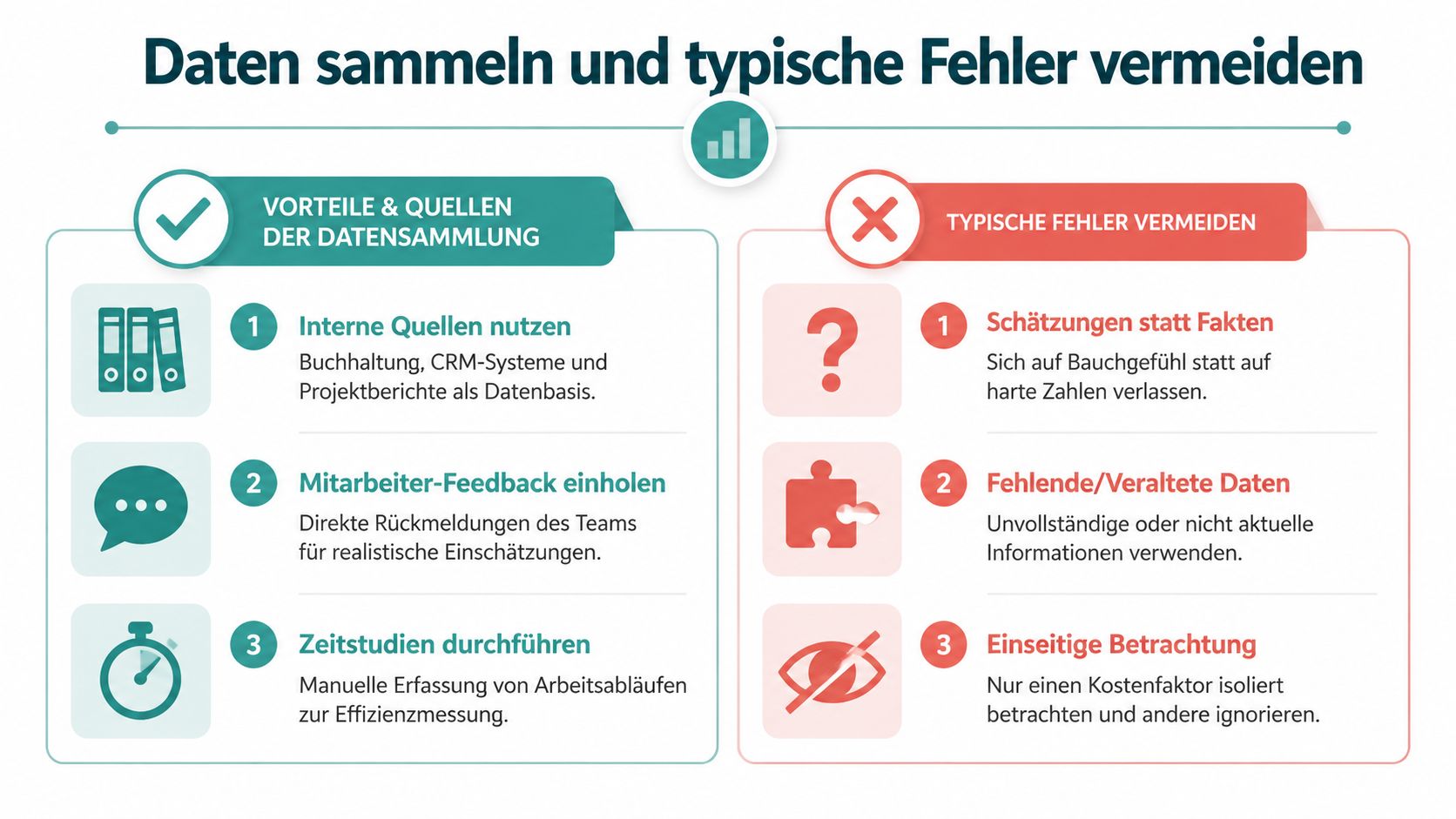

Collecting Data and Avoiding Typical Mistakes

The quality of your calculation depends almost entirely on the quality of your data. If the numbers are shaky, the whole business case falls apart at the first question.

Where to Really Find the Numbers

Most data already exists in the company. You just have to extract it from daily business.

- Payroll and HR: There you find gross salaries, employer costs, and recurring ancillary costs.

- Time tracking: Shows which roles spend how much time on planning, follow-up, or corrections.

- Dispatch and project management: Here you get the real disruptions in the process, such as rebookings, last-minute changes, and double communication.

- Financial data: Invoices for external temps, agency costs, or additional services show where spontaneous bottlenecks get expensive.

According to Vita Finance on recognizing unnecessary costs, you should document all income and expenses at least once per quarter. Especially variable costs like online subscriptions or purchases should be critically examined to identify savings potential. This idea applies directly to the company. If you only look at processes once a year, you overlook ongoing extra costs.

Mistakes That Sink Good Business Cases

Most calculation errors are not math errors. They are thinking errors.

| Typical Mistake | How to Recognize It | Better Approach |

|---|---|---|

| One-time costs missing | The calculation looks too good in year one | Include training, implementation, and internal effort |

| Only license vs. time saved | Process errors and follow-up missing | Consider the whole process |

| Estimates instead of measurement | No one can verify the number | Measure time over a fixed period |

| Recurring and one-time mixed | Savings seem permanent but are one-time | Separate clearly |

| Only one role considered | Team lead included, back office missing | Include all involved roles |

A clean solution is often simple. Measure two to four typical weeks, not just one quiet phase. Talk separately with dispatch, team lead, back office, and payroll preparation. And don’t just ask for descriptions of activities, ask to see them.

If you want data from daily business, don’t ask for opinions. Ask about the last real case.

Soft factors like less stress in the team or clearer communication can be mentioned additionally. They may support the calculation but must not replace it.

Conclusion: From Calculation to Decision

In the end, it doesn’t matter that you built a nice table. What matters is that you turn a business guess into a reliable decision. That’s exactly why the work is worth it.

How to Present Your Calculation Internally

A good template for management is concise. First show the current process with its cost blocks. Then the new process with all new costs. Then the difference, the amortization logic, and the assumptions. If someone challenges your number, you don’t have to defend it but just refer to the derivation.

Especially in events and gastronomy, an abstract tool discussion rarely convinces. Convincing is a sentence like: The current planning process unnecessarily binds leadership time, generates correction work, and makes spontaneous changes more expensive. The new process measurably reduces these costs. This is a business decision, not a matter of belief.

A useful thought also comes from completely different areas. When evaluating special offers, people don’t just look at the discount but at the actual value per use. You find exactly this mindset also at Paintball Special Offers. For your business case, this means: Don’t stare at the price of the solution but at the value of the entire new process.

If you can calculate cost savings, you get more than just budget internally. You get room to act. Because whoever can prove savings properly can also implement sensible changes.

If you want to bring your shift planning, time tracking, and payroll preparation from scattered lists and chats into a clear process, check out job.rocks. The platform supports service providers from events, gastronomy, and other personnel-intensive sectors in reducing administrative effort and managing personnel according to demand.